Reduce Your Debts with a DSA

Struggling to repay your debts? A DSA (Debt Settlement Arrangement) could be the solution. Here's how it can help:

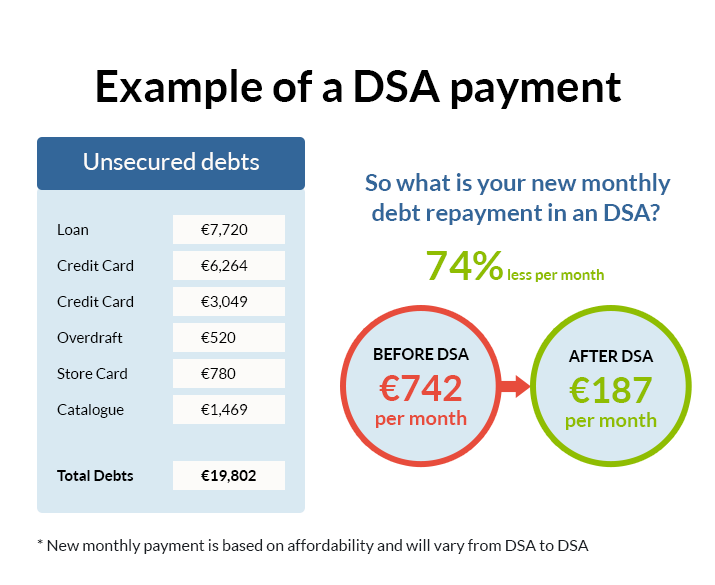

Affordable monthly payments based on what you can afford

Full legal protection from creditors

Interest & charges are frozen

Remaining debt written off on completion

Fill in the form to find out more. We will assess your situation and advise if a DSA is an option for you. We offer free, confidential, no obligation advice.

Find out if you qualify

How does a DSA work?

Firstly, you have a chat with one of our advisors to see if it is your best option. We analyse your financial situation and work out what you can realistically afford to pay to your creditors, after giving priority to your other expenses. We discuss everything in detail, including all of your options. If you decide to proceed with a DSA, our PIP's (Personal Insolvency Practitioners) can start working on your DSA.

Once the Insolvency Service of Ireland (ISI), the courts and your creditors have all agreed to your DSA, it becomes legally binding and you can start your lower repayments. After 60 months (usual term of an DSA), you are free of your debts and any remaining unpaid debt is written off.

The need to knows

-

Who can do a DSA?

Almost anyone who is in financial difficulty with unsecured debts (credit cards, loans, overdrafts, etc...) can do a Debt Settlement Arrangement. You can be single, married, employed, self-employed, a homeowner or a tenant...

There are certain criteria involved in order to do a Debt Settlement Arrangement, such as debt level and number of creditors, but we can discuss this further when we chat. If a DSA is not suitable, we can recommend other various options for you to consider.

-

How is my payment calculated?

Your DSA payment is calculated by analysing your income and expenses on a monthly basis (not including any debt repayments). We then work out how much money you have left over each month. This left over amount is your potential DSA payment.

-

About our company

McCambridge Duffy have helped 1,000s of people with their debts over the years. We are a leading provider of Insolvency solutions and have been in business for over 80 years. We have a great reputation for the service we provide to our clients and also among all the major lenders.

Why choose McCambridge Duffy?

1) No upfront fees - Saving you time and money

We are one of the only companies who do not charge upfront fees. Paying any provider upfront fees will only cause a delay in your DSA being accepted and cost you extra money that is completely unnecessary. If your DSA is rejected you will lose this money. DO NOT PAY UPFRONT FEES EVER!

2) High acceptance rate

We have an amazing acceptance rate for DSA's proposed. We know any DSA's we propose will have a great chance of being accepted. We also fight very hard for every client to make sure their DSA proposal is carefully considered by the creditors. Our proposals will always be based on something that is affordable and because of this every DSA we propose will be unique.

3) Excellent Customer Service

We have an excellent customer care team. We are a family run company and our advisors have all been with us for many years. They are highly trained and will be able to answer any question quickly and professionally. You will also find us very friendly.

Our Philosophy

At McCambridge Duffy we believe that...

"Every problem has a solution."

We believe that everyone should have access to sound advice, information and the best possible options for their situation. We pride ourselves on offering good quality, caring customer service.

Our philosophy is reflected in the feedback we receive from our many happy clients and the results in the successful plans we put forward. Read some of our testimonials below taken from our many client reviews.

Client Testimonials

-

General Debt Advice

We offer a free advice only service where we can review your financial situation and let you know of all of your options.

-

PIAs

We also offer Personal Insolvency Arrangements (PIAs) - a way of formally dealing with mortgage and unsecured debts.

-

Bankruptcy

If Bankruptcy is your only option, we also offer a Bankruptcy service where we can guide you through the process.

What is a Debt Settlement Arrangement?

You can enter a Debt Settlement Arrangement with your creditors when you are considered insolvent. You are considered insolvent when you are unable to pay your debts in full and as of when they fall due.

A DSA will only include unsecured debts; there is no limit to the amount of unsecured debt when entering a DSA. There are certain unsecured debts that cannot be included in a DSA and certain unsecured debts require the consent of the creditor before it is entered into a DSA. Secured Debts such as Mortgages cannot be included in a DSA.

Unsecured Debts are Debts where the creditor does not have the ability to seize specific assets belonging to the debtor should repayments not be maintained. A Debt Settlement Arrangement will begin when you and 65% of your creditors (in value) agree to the proposal put forward by the Personal Insolvency Practitioner (“PIP”).

Under the DSA, your unsecured debts will be settled over a period of 5 years, with the possible extension of an additional year in certain circumstances, resulting in a DSA lasting 6 years.

Once the DSA has been successfully completed, you will be discharged from the remainder of your debt at the end of the period.

What are the criteria for a DSA ?

You are considered suitable for a DSA if you meet the following conditions

- You are insolvent and unable to pay your debts in full as they fall due.

- You have a total of one or more more unsecured creditors.

- Your domicile must be in the Republic of Ireland or you must have, within the past year, ordinarily resided or had a place of business in the Republic of Ireland.

- You have completed a prescribed financial statement (PFS) and signed the statutory declaration stating that it is both true and accurate.

- You have obtained a statement from the Personal Insolvency Practitioner, that they are of the opinion that:

- The information in the PFS is true and accurate.

- You are eligible to make a proposal for a DSA; and

- Having considered the PFS, they are of the opinion that you will not be solvent in the next 5 years.

- Having considered the PFS, they are of the opinion that you will not be solvent in the next 5 years.

- Having considered all possible options, a DSA is the best solution for you and that there is reasonable prospect that you will become solvent upon completion of the DSA.

Criteria that might prevent you from getting a DSA

You are not eligible to seek a DSA should the following requirements apply

- You have incurred 25% or more of your unsecured debts within the past 6 months.

- You have been subject of a Debt Relief Notice now, or within the past 3 years.

- You must not be the subject of a Personal Insolvency Arrangement now, or within the past 5 years.

- You have been the subject of a DSA before. (With Exceptions)

- You are currently bankrupt, subject to a bankruptcy measure or have been discharged from Bankruptcy in the past 5 years.

- You have been the subject of Protective Certificate issued in respect of a DS A within the last year

What type of debts may or may not be included in a DSA?

- Personal Loans

- Credit Union Loans

- Business / Commercial Loans

- Store Cards

- Overdrafts

- Personal Guarantees (Liquidated and Called up)

Debts that can be included only with creditor consent

- Taxes, duties, levies owed or payable to the state

- Local Government charges

- Amounts due to the Health Executive under the Nursing Home Support Scheme

- Annual service charges to owner’s management companies ( Apartments and Housing estates)

- Liabilities arising under the Social Welfare Consolidation Act 2005 Local Authority Rates

- Household Charges

Debts that cannot be included in a DSA

- Family maintenance payments under court orders

- Court fines in respect of criminal offences.

- Liabilities arising out of injury or wrongful death claims awarded by the Court

- Liabilities arising from loans obtained by Fraud

- Secured Debts

Find out if a DSA is right for you

The simplest way to find out if a Debt Settlement Arrangement is right for you is to have a chat with us.

Enquire about a DSA