A PIA ( Personal Insolvency Arrangement) is a formal debt solution that might be suitable if you are having difficulty repaying your mortgage and other debts. A PIA can also help if you are dealing with mortgage arrears. The purpose of a PIA is to help you remain in your home.

A Personal Insolvency Arrangement is a great solution if your financial difficulties are mainly caused by mortgage arrears or unaffordable mortgage payments as well as payments on loans and credit cards. The main purpose of a PIA is to allow you to regain control over your financial affairs in a way that is fair and realistic for you and your creditors, whilst allowing you to keep your home.

The first thing we do when you get in touch is have a chat to see what all of your options are to addressing your debts. We will analyse your living situation, your mortgage and your debts and work out what you can realistically afford to pay towards your debts and mortgage each month, after giving priority to your other living expenses.

In order to reduce your monthly mortgage repayments your mortgage lender can agree to do one of or a combination of the following, depending on what your circumstances are:

You negotiate affordable lower monthly repayments towards your unsecured debts (credit cards, loans etc...) which usually last for the term of your Arrangement (72 months) or sometimes shorter depending on your circumstances. Interest and charges are frozen. On completion of the arrangement, any remaining unsecured debts are written off.

If you would like to find out more about a Personal Insolvency Arrangement or to find out what other options are available, click here to fill in the form and one of our advisors will call you for free, confidential consultation.

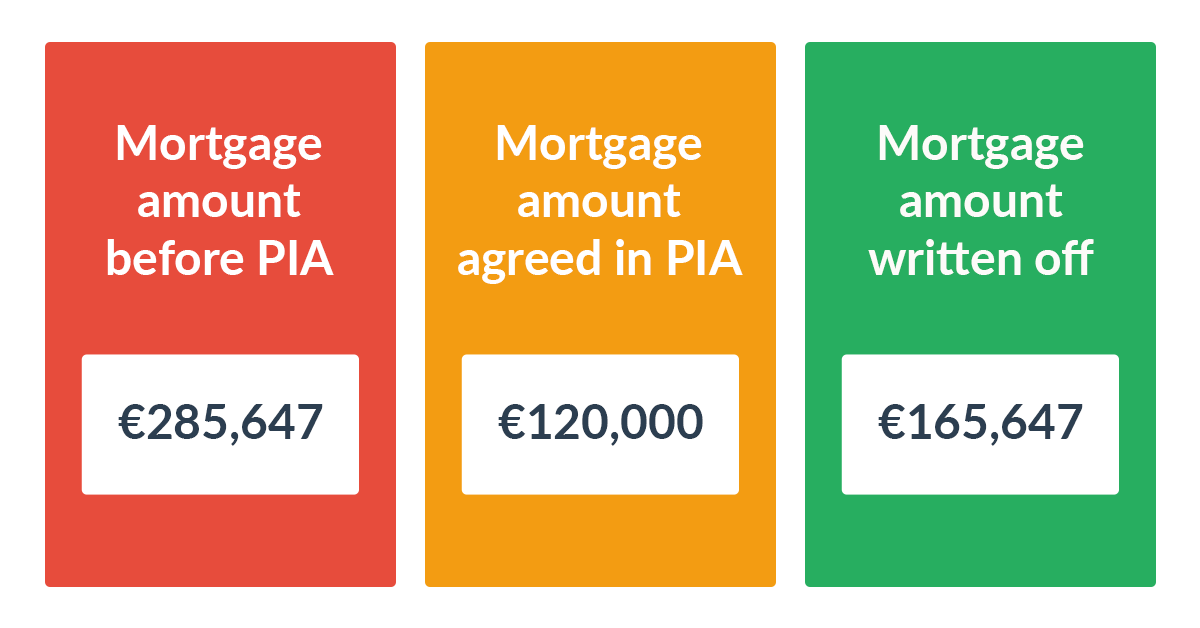

Below is an example of one our actual PIA cases. Our clients, a married couple with 3 children, ran into financial difficulty after going through a period of incapacity and unemployment. Contractual payments on their mortgage and other debts became difficult to manage during this time. Mortgage arrears started to build and they contacted us for advice. After assessing their situation, it was determined that a PIA might be a suitable option to help address their financial problems. After careful consideration they decided to proceed with a PIA. Their PIA was successfully approved. Below is a breakdown of how their PIA was structured.

Contact us for a free consultation. We will discuss you situation and explain what options you have available for addressing your debts. If you wish to proceed with a PIA with McCambridge Duffy, then we will draft your Prescribed Financial Statement (PFS) and you will progress to the next stage of Protective Certificate (PC) application.

Our PIP submits your application to the ISI and court. If they are happy, your Protective Certificate will be granted. The PC stops creditors from taking action against you for a specified period oftime. Your PIP will begin drafting your PIA proposal for the creditors.

Your proposal is sent to creditors for voting in a "meeting of Creditors". At least 65% of the creditors (50% of both secured and unsecured) must vote in favour of the proposal in order for it to be approved.

The Insolvency Service of Ireland (ISI) and the Court carry out a final review. If they approve everything, your PIA will become legally binding. Your new payments and plan for addressing your debts can begin. If the PIA proposal is rejected, you may be eligible to appeal for a Court review in order to try and overturn the rejection.

Your case manager and PIP will oversee your PIA, to ensure everything runs smoothly. Your case manager will be available to deal with any queries you might have and will carry out annual reviews during the term of the PIA. On successful completion, unsecured debts are written off and secured debts will be dealt with as agreed in the terms of the PIA.

You can enter a Personal Insolvency Arrangement with your creditors when you are considered insolvent. You are considered insolvent when you are unable to pay your debts in full and as of when they fall due. You can be single, married, employed, self-employed, a homeowner etc...

There are certain criteria involved in order to be elligible for a Personal Insolvency Arrangement, such as mortgage outstanding, mortgage amount, mortgage interest, debt level and number of creditors, but we can discuss this further when we chat. If a PIA is not suitable, we can recommend other various options for you to consider.

Your payments are calculated by analysing your income and expenses on a monthly basis (not including any debt or mortgage payments). We determine how much money you have left over to go towards your mortgage and your debts. The amount of that money that goes towards your mortgage and the amount of that money that goes towards your debts is entirely dependent on your mortgage situation and the amount of debt you owe.

The types of debts that can be included are:

Not all of your creditors have to agree to your proposal in order for it to be approved. At least 65% of your total creditors (at least 50% secured and 50% unsecured) in terms of value must vote in favour of your proposal in order to make it binding on all of your creditors.

You are considered suitable for a PIA if you meet the following conditions:

You are not eligible to seek a PIA should the following requirements apply:

Your lower repayments will commence. We will assign dedicated case managers who will look after you and your PIA for it's duration. Your case manager will be there to answer any queries you might have throughout the term of the PIA. When your PIA is complete you will be discharged from any outstanding balances on your unsecured debts. You may be released from your secured debts or you may continue to pay these, depending on the terms of the agreement.

Unlike most other Insolvency providers, we do not charge for our advice and we do not charge upfront fees as we believe this to be unethical. You will never receive a bill from us.

Only if your PIA is accepted will we receive any payments for fees for managing your case. If your PIA is not accepted then you pay nothing. Our fees vary depending on your circumstances and they are built into your affordable monthly payment to your creditors. All of this is clearly explained when you chat to us. It is your creditors who determine what we get paid and we cannot draw fees without their approval.

There are range of Personal Insolvency solutions available in Ireland that all help deal with different kinds of debt. Browse the solutions below or contact us to find out your options.

A Debt Settlement Arrangement (DSA) is a formal solution that addresses unsecured debts, such as credit cards, loans, overdrafts etc... In a DSA, you affordable repayments are negotiated with your creditors. Any remaining unsecured debt is written off on completion.

If you are struggling with debts similar to that mentioned above, then a DSA might be a suitable option for you.

Click the button to read more about a DSA, or contact us for a free and confidential consultation and we will advise on your options.

A Debt Relief Notice (DRN) is a formal solution designed to help people who cannot afford to pay their unsecured debts, are on a low income and have little to no assets. A DRN is sometimes referred to as a form of 'mini-bankruptcy'. A DRN usually lasts for about 3 years and debts are written off on completion.

If you meet the criteria above and your total debts are not above €35,000, then a DRN might be a suitable solution for you.

Click the button to find out more about a DRN, or contact us for a free and confidential consultation today.

Bankruptcy is a formal procedure that deals with unaffordable secured and/or unsecured debts over the amount of €20,000. It is usually considered as a last resort option and you have to investigate the other available Insolvency solutions, before you can go down the Bankruptcy route. Bankruptcy usually lasts for one year and debts are written off on completion.

If you cannot repay your debts and have been deemed unsuitable for the other insolvency options, then Bankruptcy might be your only remaining option.

Click the button to read more about Bankruptcy, or contact us for a free and confidential consultation and find out your options today.

There are situations where a formal insolvency solution may not be necessary to address financial difficulties. In some cases, an informal arrangement with creditors may be more suitable, allowing you to manage your debts without the formalities and potential limitations of insolvency proceedings. Informal arrangements often provide the flexibility to negotiate directly with creditors, offering a tailored approach that may involve partial debt repayment, an extended timeline or a plan to sell assets in order to discharge creditors in full.

We take a comprehensive approach, assessing your financial circumstances and exploring all available options. Our experienced team carefully evaluates the advantages and disadvantages of both formal and informal solutions, ensuring that you understand the best course of action for your situation. By focusing on a customised strategy, we can often help you achieve debt relief through informal agreements when possible. Click the button and fill in the form for free and confidential advice on your options.

If you are experiencing difficulty with debt (secured or unsecured), but aren't sure what to do about it, then you might like some general advice. Our experienced advisors provide a listening ear and expert advice, so you can gain some clarity on how to deal with the situation.

This service is completely free of charge and will give you the knowledge required to make a suitable choice. If we cannot help you with any of our solutions, we will signpost you to an appropriate provider or charity that can help, such as the Money Advice and Budgeting service (MABS).

Click the button and fill in the form for free and confidential advice on your options..